In the UK’s dynamic finance market, individuals and businesses encounter two main routes to get help. One is contacting a direct lender; the other is contacting a lender through a broker. While both entities operate differently and offer distinct advantages, understanding when to contact each helps. Choosing one between them depends on your financial preferences and goals.

What is a direct lender?

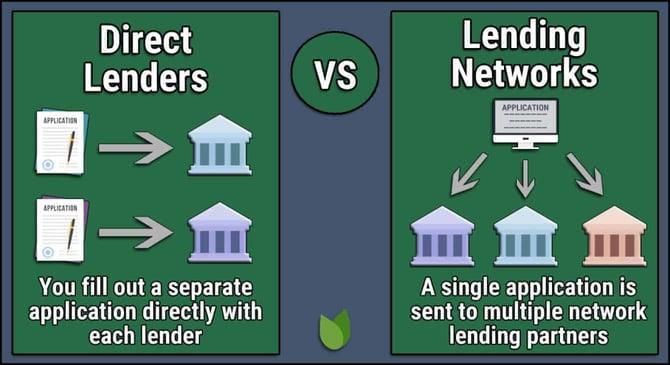

A direct lender is an independently operating financial institution that provides and manages the loan itself. They help a borrower from making the application to getting the cash.

Yes, direct lenders are the ones who provide the loan amount after analysing affordability against set parameters. In this, a borrower deals directly with a loan or associated issues. Thus, it may help the person reschedule payments or seek better repayment options without making details vulnerable.

What are the Key characteristics of a direct lender?

- Control and simplicity: The process is streamlined and simple because only one organisation handles everything.

- Direct pricing: You generally pay the fees associated with the loan directly to the lender in the form of loan payments. It does not call for intermediary markups

- Speedy decisions: With fewer parties involved, direct lenders may offer quick decisions. If you already have an account with one, you may be able to get the loan more quickly.

- Limited market exposure: Direct lenders do not copy other products. Instead, walk by their beliefs and their product line. Hence, unique and customer-friendly terms prove beneficial for the borrower.

When should I choose a direct lender?

You should choose a direct lender when you need money urgently and cannot wait more than 24 hours. Here is when choosing a direct lender is favourable:

- Strong Credit Profile: Individuals with a good credit rating may get instant approval and better terms. You may even qualify for the advertised rates, far lower than the actual ones.

However, there is little complexity to getting loans for bad credit from a direct lender in the UK marketplace. You may not qualify with every loan provider if you have a poor credit rating. Your choices remain bare minimum in this case. However, contacting a direct lending company that deals especially in such profiles may prove helpful. - You know the loan you want: You can choose a direct lender if you know the loan type and have compared rates already. You are confident that a specific loan company offers the lowest rate. It helps you avoid intermediary fees.

- You want to keep matters private: You may prefer a direct lender if you want one single point of communication instead of going via a broker. The loan companies manage all your queries and documentation.

- You want to avoid brokers: they receive a commission from the respective lender. However, you can avoid the fee if you deal directly with the direct lender. They do not charge any upfront fees.

What is a loan broker?

A broker acts as a middleman between a borrower and a direct lender. It only helps suggest the best loan provider by analysing the borrower’s needs and financial situation. It does not provide the loan or cash directly to the borrower.

Brokers work with a personal panel of direct lenders. The number may even cross 100, and it helps you find the best one for your situation. They discuss your requirements on your behalf and help with documentation.

What are the Key characteristics of a loan broker?

A loan broker (also referred to as a credit broker or intermediary) is defined by a specific set of professional, operational, and regulatory characteristics. Understanding these traits helps borrowers assess the value a broker can add and distinguish high-quality brokers from basic lead generators.

Below are the key characteristics of a loan broker.

- Intermediary, not a lender: A loan broker does not lend money. Instead, they act as a matchmaker between lenders and borrowers. It facilitates introduction, applications and negotiations. The broker’s role is advisory and facilitative, not credit providing. Final lending decisions always rest with the lender.

- Access to Multiple lenders: Brokers share a panel of direct lenders, ranging from a handful to several hundred. Panel can include high-street lenders, challenger banks, specialist and non-prime lenders, and private and alternative finance providers.

- An authorised and regularised broker: A broker should be authorised and regulated by the Financial Conduct Authority for credit broking. It complies with the Consumer Credit Act and the Treating Customers Fairly (TCF) requirements.

- Advisory and suitability Role: A professional broker helps save time by checking your affordability and connecting you with the right and affordable loan company. It also helps you identify he borrowing objectives and risk factors.

- Problem-solving ability: A broker’s expertise proves most important for individuals with a chequered credit history, non-standard income, and complex loan structures. You may find the best direct lender providing loans for bad credit profiles.

When Should You Choose a Loan Broker?

Here are some situations where choosing a loan broker may prove helpful :

- Problematic credit profile: You can consider a broker if your credit profile is non-standard. It means that if your profile has issues like CCJs, missed payments, or loan defaults, a broker may be helpful. They help you partner with the most tolerant firm. It avoids unnecessary declines and credit score damage.

- Complex income: Your income is highly complex if you are a self-employed, part-time worker or a gig employee. A broker shares the expertise in helping you partner with a loan company with whom you share high chances of qualifying for a loan.

- Compare multiple lenders: If you want to compare multiple lenders before choosing one, a broker may help. The person may help you get results quickly. Alternatively, you can contact them if you are not sure about your loan choice or a direct lender.

- Specialised loan requirement: Sometimes, your loan requirement requires specialisation. For example, in the case of bridging finance, a company should seek a broker’s assistance. It helps them navigate the process and documentation. A broker may also tell you about the loan company’s discretion.

- You want someone to manage the process: If you are new to the borrowing world, a broker may help. He may help you find the right loan lender and navigate the application and documentation process. It thus eases the process of getting a loan.

How to choose the right route: Explain in Brief

The table may help you understand the best time to approach a broker or a direct lender.

| Scenario | Best Option |

| You have excellent credit and know your product | Direct lender |

| Your situation is complex (e.g., self-employed, non-standard income) | Broker |

| First-time borrower seeking multiple options | Broker |

| You want the fastest possible decision. | Direct lender |

| You want to explore competitive pricing across lenders | Broker |

Conclusion

Whether you choose a direct lender or a broker should depend on your credit profile. It depends on the complexity of your needs. Check whether access to a broader lender market matters more than a direct, streamlined process. Use your specific financial goals to guide your choice, and always verify authorisation before committing to a loan arrangement.

If you would like help choosing loan options based on your credit profile or financial goals (e.g., mortgages, business loans, bridging finance), contact experts.

Hi everyone, I am Lukas Thomas. I am a professional writer and author with having specialisation in the UK financial sector. I have more than 13 years of experience as the financial writer and hope it will continue longer. I have done my post-graduation in Masters of Business Administration (MBA) in Finance. Currently, I am performing my responsibility as a Senior Loan Expert in CashLoans2go, which is the fastest-growing online direct lending company. My job is to prepare borrower-friendly loan deals as per the company’s guidelines. I also write research-based blogs for the company’s official website. You can read them and gain knowledge on any loan product.