Financial difficulties can affect most of us at some point in life. But what if your credit score looks more like a cricket score than a football one? Many lenders slam doors shut when they see poor credit histories. They want proof you’ll pay them back, which makes it harder to show.

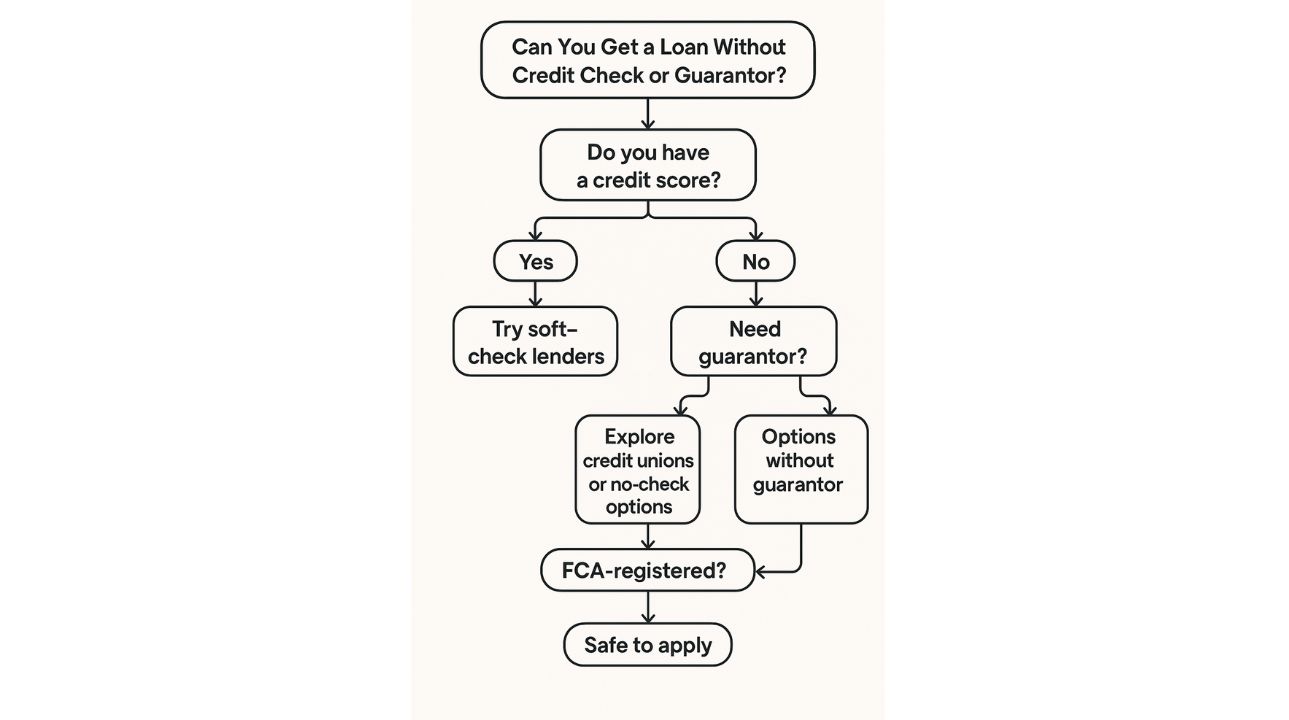

Many banks won’t look twice at loan forms that lack a guarantor’s name. They want that safety net of another person who’ll pay if you can’t. This gap has pushed some lenders to create new loan types. They focus less on what went wrong before and more on your current money flow. These companies conduct soft checks that review basic information.

The no guarantor loans can help you with your situation. You make sure to pay it off as soon as possible without stretching the loan period. You just have to find the right direct lender to get this loan. Learn how you can tackle these loans.

Who Needs These Loans?

untain. Many people with poor or zero credit scores turn to no guarantor loans for help. They often can’t get normal bank loans because lenders see them as too risky. People without anyone to back them up face extra hurdles. Some feel awkward asking someone to take on financial risk for them.

Part-time workers and those between jobs struggle even more. Traditional lenders want steady income proof before they’ll hand over cash. These special loans might be your only shot at the needed funds.

Do you need money quickly? You can get long-term loans with an instant decision and cut through endless waiting. Some lenders now give answers in minutes instead of days. This helps when life throws unexpected bills your way without warning.

The past financial mistakes haunt many borrowers for years. CCJs and defaults stick to your record like glue. Most high street banks slam doors shut if they spot these marks. These loans look beyond old problems to your current ability to pay.

The fees tend to run higher than regular loans. But when you need cash and have nowhere else to turn, they fill a real gap. You check the total cost before signing, and be sure you can manage the monthly payments.

Can You Really Get Loans with No Credit Check and No Guarantor?

The truth about “no credit check” loans isn’t what most ads claim. Almost every lender runs some form of check on new clients. Soft checks peek at basic details without leaving marks on your file. Many loan companies use these lighter checks as a first step. They see enough to make choices without the full dive that hurts your score.

Hard checks show up on your record and can drop your score. This stays visible to other lenders for months or years. Some companies focus on just your own money status right now. They care more about your current job and bank flow.

The FCA keeps tight reins on all lenders to shield people from harm. Their rules make true “no check” loans nearly extinct in the legal market. Any firm that skips all checks likely breaks these rules.

Worth Knowing

- Most “no check” claims hide the fact that some review happens

- Interest rates jump sharply as checks get lighter

- Payday companies often use limited checks but charge huge fees

- Online-only lenders may offer quicker decisions with fewer hurdles

- Always check for the FCA logo before sharing your details

The monthly costs climb much higher than standard bank loans. You can weigh this price against your need for quick money.

How These Loans Compare by Term Length?

| Term Length | Loan Type Commonly Used | Pros | Cons |

| Under 3 months | Payday, BNPL | Fast, flexible | Very high interest |

| 3–12 months | Instalment loans | Manageable repayments | Still expensive |

| 1–3 years | Personal loans | Spread cost further | May need steady income |

| 3+ years | Secured loans | Larger sums possible | Risk losing asset |

Loan Types For You

You have more options than you might think. These five loan types help folks who can’t pass tough checks or find someone to back them.

1. Personal Instalment Loans

These loans spread your payments over months or even years. Many lenders use just a soft check that won’t harm your score. You’ll get a fixed sum upfront and pay back in set chunks. The rates start around 30% APR but can reach 100% for bad credit. Some companies give answers in hours, not days.

2. Secured Loans Against Assets

You can use your asset as backup for a loan. The lender knows they can take your stuff if you don’t pay. This makes them more likely to say yes despite poor credit. The risk falls on you, but rates stay lower than other options.

3. Credit Union Borrowing

Local credit unions offer small loans from £500 to £3,000 at fair rates. Most charge about 3% monthly, much less than quick-cash companies. You’ll need to join first and sometimes save for a few weeks.

4. Buy Now, Pay Later Services

BNPL lets you take home goods today. You pay in small payments over weeks or months instead of all at once. Many shops offer this at checkout, both online and in stores. Some plans charge no extra if you pay on time.

5. Peer-to-Peer Options

These connect you directly with people willing to lend their cash. Some P2P sites work with low credit histories. The terms often beat what banks offer for similar risk levels.

Steps to Get One Safely

You follow these five steps to find money help without falling into traps that could cost you dearly.

Step 1: Always check if a lender shows the Financial Conduct Authority logo. Every legal loan company must have FCA approval to operate. Their website should display a firm number you can verify. The FCA register lets you search these numbers online for free. You can avoid any company missing from this official list.

Step 2: You can look past flashy “low monthly payment” ads to find the price. The APR tells you what you’ll pay over a whole year. Many bad-credit loans charge between 49.9% and 1500% APR. You can check for hidden fees like setup costs or early payoff charges. A £1,000 loan could cost £2,000+ by the end.

Step 3: Many good lenders tell you upfront what kind of credit check they’ll run. Soft checks won’t harm your score even if you’re turned down. Hard checks leave marks that other lenders can see for months.

Step 4: You don’t have to pay money to get a loan. The lenders take their cut from the loan itself. Any “broker fee” or “admin charge” before approval is likely a scam. These companies often take your cash and vanish without a trace.

Step 5: You can check what other borrowers say about the lender. Many sites show customer feedback. You can look for patterns in complaints about hidden fees or poor service.

Conclusion

You might have some choices when looking for loans, no guarantor or no credit checks. Most places do at least a minimum check, but some care more about how much money you have right now instead of past failures.

But this help comes at a cost, a cost that accumulates over time. That way, you will never be surprised as to the full cost of anything before you sign any deal. These loans pick up the pieces for short-term money cracks.

Hi everyone, I am Lukas Thomas. I am a professional writer and author with having specialisation in the UK financial sector. I have more than 13 years of experience as the financial writer and hope it will continue longer. I have done my post-graduation in Masters of Business Administration (MBA) in Finance. Currently, I am performing my responsibility as a Senior Loan Expert in CashLoans2go, which is the fastest-growing online direct lending company. My job is to prepare borrower-friendly loan deals as per the company’s guidelines. I also write research-based blogs for the company’s official website. You can read them and gain knowledge on any loan product.