Home credit opens money assistance right in the living room. The entire transaction occurs in the comfort of your home, and you do not need to wear suits to have those bank meetings. Many offer doorstep loans with no credit checks from a direct lender, looking at your current financial picture instead of past mistakes.

You pick how to pay back. The majority of them select weekly visits with an agent. Other businesses are currently selling plans every month, in case that fits your budget needs better. These loans are spent by many borrowers on the washing machine when it becomes inoperable or when their school-going kids have school breaks. The amounts match these everyday needs rather than big spending dreams.

What is Home Credit / Doorstep Lending?

Home credit, also known as doorstep lending, brings financial services right to your doorstep. The lenders send agents to your home to offer loans and later collect weekly payments. These loans range from £100 to £2,000 for small needs.

The process starts when a representative visits to discuss your needs and assess if you can afford repayments. They explain the terms clearly before any papers are signed. Many people choose doorstep loans with no credit checks from a direct lender because approval often depends more on your current situation than past credit history.

Home credit targets households with modest incomes who might struggle with mainstream banking. The convenience of in-person service appeals to those who prefer cash handling or face-to-face talks about money.

How Does Home Credit Work?

A home credit loan starts with a simple application process. You may contact lenders via the internet or use the phone and talk with a local agent. Most individuals like face-to-face communication about their financial needs instead of completing forms.

After you apply, the waiting time is short. Most lenders make decisions within hours, not days. They look at your income and spending habits instead of just credit scores. They sit down with you and go through every detail. You’ll know exactly what you’re signing up for.

The agent hands you cash right there when the loan is approved. There is no waiting for bank transfers or checks to clear. The money is yours to use straight away.

The repayment works on a weekly schedule that fits with how many people budget. The same agent drops by each week to collect what you owe. This regular contact builds trust between borrower and lender.

| Pros and Cons of Home Credit Loans | |

| Pros | Cons |

| Easy and fast access to cash | High interest rates and fees |

| Flexible repayment schedules (weekly/monthly) | Risk of falling into a debt cycle |

| No complex paperwork or online application needed | Agents visit home (privacy concerns) |

| Suitable for people with poor or no credit history | Limited loan amounts (£100–£2,000) |

| Personalised customer service at the doorstep | Less transparency than online lenders |

| Quick approval process | Late repayment penalties can add up |

| Can help in emergencies or small purchases | Total repayment may be double the borrowed amount |

Eligibility & Application Process

Doorstep loans open doors for many who find banks too strict. You don’t need a spotless money history to qualify. You must be at least 18 years old and live in the UK. The lender will need to see where you live. You have to bring a recent bill with your name and address.

You can bring along your ID, like a driver’s license or passport. Most companies want proof that you can pay back the loan. This might be pay slips, bank statements, or benefit letters. Some lenders don’t insist on a bank account, which helps folks who use cash day to day.

The agents do quick checks on who you are and if you can afford payments. They look at what money comes in and goes out each month. Many people hear “yes” or “no” while the agent is still there. If approved, you could have cash in hand that same day.

Customer Rights & Regulations

The UK takes firm steps to shield borrowers using doorstep loans. Since 2014, the Financial Conduct Authority has watched over all home credit firms. The lenders must follow strict rules or lose their license to do business.

As a customer, you have clear rights when taking out these loans. The total loan cost, weekly payment amount, and loan length should be clear. You can walk away from any home credit deal within 14 days without giving reasons. This cooling-off period lets you change your mind if you have second thoughts.

You can speak up if things go wrong with your loan. The lender must handle your worries fairly and give answers within eight weeks. You can take your case to the Financial Ombudsman Service at no cost.

The agents must treat you with respect and never push you to borrow more. They can’t visit your home at odd hours or use harsh talk to collect payments.

| Advantages by Customer Type | |

| Low-income households | Easy access without bank hurdles |

| People with poor credit | No perfect credit needed |

| Seniors | Personalized doorstep service |

| Short-term borrowers | Quick cash for urgent needs |

| Users needing guidance | Agent explains terms clearly |

Who Should Use Home Credit Loans?

Home credit loans serve people whom banks don’t approve of. These loans could be your lifeline when cash runs short if your credit score has taken some hits.

Many users turn to doorstep loans during sudden money troubles. The quick approval and cash-in-hand approach solves urgent needs without long delays. These loans work well for smaller buys that can’t wait until payday. Perhaps your child needs school supplies or winter boots as the weather turns cold. The amounts offered match these kinds of modest but needed expenses.

People who work in cash jobs often struggle with bank paperwork. Self-employed painters, market traders, and seasonal workers may find doorstep lenders more willing to see their financial situation. The face-to-face chats let you explain your case in ways forms cannot.

Some borrowers simply prefer dealing with actual people rather than online forms or bank machines. The weekly visits create a rhythm and reminder to help with budgeting for many households.

Alternatives to Home Credit in the UK

Before signing up for doorstep loans, it’s worth checking other money options.

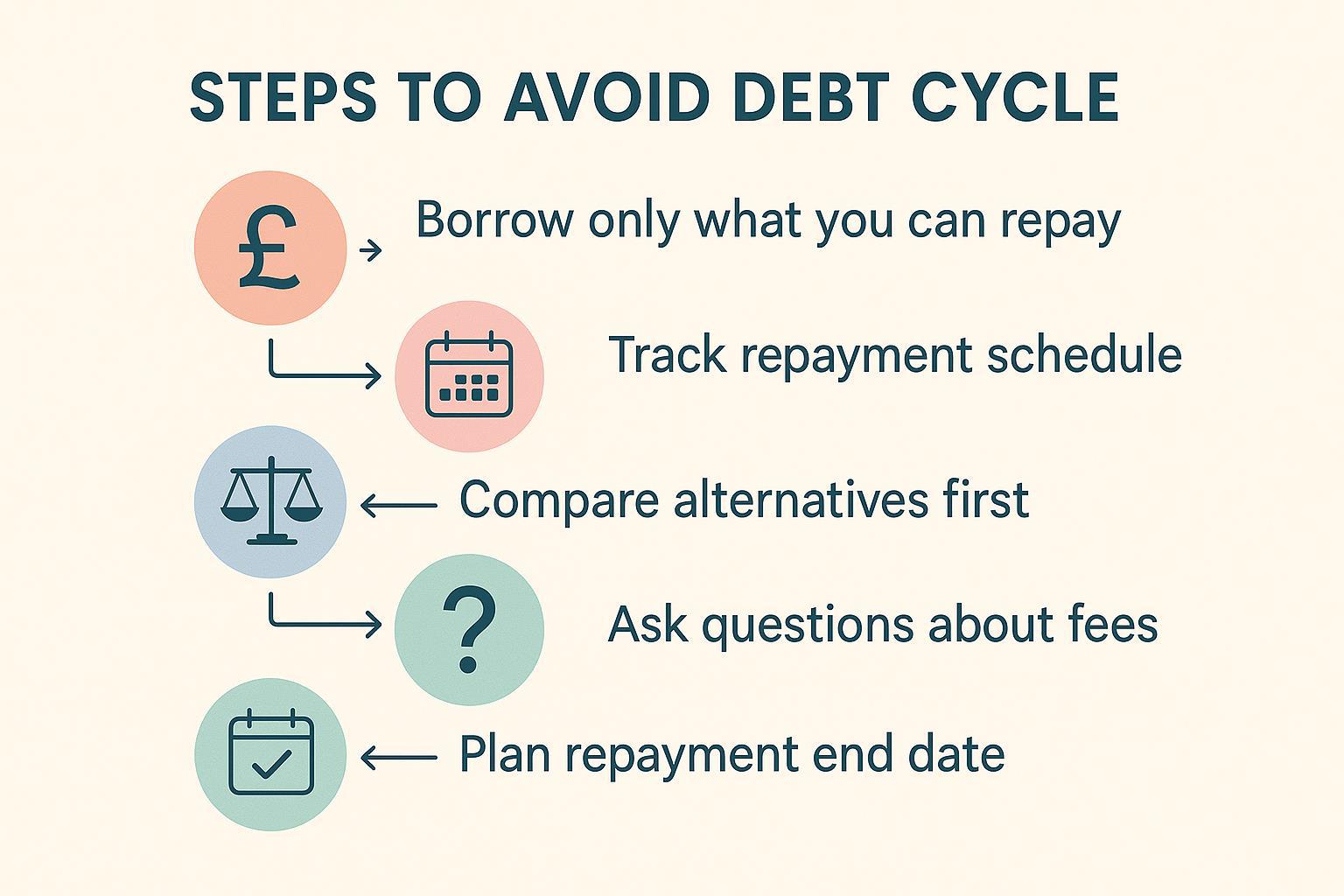

- Credit Unions – These are non-profit-making groups that manage loans at very friendly rates. Members collectively save and subsequently borrow out of the joint pot. Most of them limit the interest charged to 3 per cent per month, much lower than the rate charged by home credit. First, you will have to join and save some time.

- Payday Loans – These are the emergency financial providers that provide money till your next paycheck. The money gets into your wallet within hours upon the completion of a simple online form. The rate of annual interest may exceed 1,000%.

- Bank and Online Lenders – These are the banks that you can use should your credit not be too shaky. The internet lenders have become very understanding of small credit lapses. You would be saving on the interest charged on doorstep loans.

- Family Borrowing – You can ask loved ones for help. Write down what you both agree to avoid later problems.

- Shop Now, Pay Later – Many stores let you take items home and pay in small payments. These plans work well for single buys like beds or phones.

Conclusion

Home credit does not suit everybody, but it satisfies an actual need. You have a chance to balance the increased expenses with the convenience and quickness, as with any financial option. You never put on the mortgage a sum of money that you cannot easily recover by that weekly collection at the doorstep.

Hi everyone, I am Lukas Thomas. I am a professional writer and author with having specialisation in the UK financial sector. I have more than 13 years of experience as the financial writer and hope it will continue longer. I have done my post-graduation in Masters of Business Administration (MBA) in Finance. Currently, I am performing my responsibility as a Senior Loan Expert in CashLoans2go, which is the fastest-growing online direct lending company. My job is to prepare borrower-friendly loan deals as per the company’s guidelines. I also write research-based blogs for the company’s official website. You can read them and gain knowledge on any loan product.